How To Use This Calculator

Fill in the fields below and hit the calculate button. Also choose any of our additional options to customize your calculation to better fit your specific loan scenario. Once you submit, your monthly payment will be calculated and displayed along with the total interest paid over the life of the loan and a full amortization schedule showing each payment broken down by principal and interest.

Tip: Click the question mark icon () next to any field for more information.

Calculator Fields

Commercial Loan Payment Summary

| Summary | |

|---|---|

| Principal + Interest Payment | $5,995.51 |

| Number of Payments | 360 |

| Periodic Interest Rate | 0.500% |

| Total Payments | $2,158,379.01 |

| Total Interest | $1,158,379.01 |

Commercial Loan Amortization Schedule

| # | Payment | Interest | Principal | Balance |

|---|

Commercial Mortgage Payments Graph

Current Commercial Mortgage Rates

Not sure what interest rates to use? Start with the average commercial mortgage rates below, organized by loan and property type. These rates were updated August 8, 2026

Loan Types

| Commercial Loan Type | Average Rates |

|---|---|

| Conventional | 5.55% - 8.90% |

| Private Banking | 5.88% - 8.75% |

| SBA 7A | 5.75% - 8.75% |

| SBA 504 | 6.19% - 6.28% |

| USDA | 6.00% - 8.75% |

| Insurance | 5.85% - 8.95% |

| CMBS | 6.35% - 8.15% |

| Bridge | 5.75% - 12.75% |

| Construction | 5.50% - 8.75% |

| Mezzanine | 7.07% - 12.23% |

Real Estate Types

| Commercial Loan Type | Average Rates |

|---|---|

| Office | 5.50% - 12.75% |

| Retail Center | 5.50% - 12.75% |

| Industrial | 5.50% - 12.75% |

| Hospital & Healthcare | 5.23% - 8.90% |

| Self-Storage | 5.50% - 12.75% |

| Hotel | 5.55% - 12.75% |

| Mixed Use | 5.50% - 12.75% |

| Churches | 5.50% - 12.75% |

| Multifamily | Apartment Loan Rates |

Commercial Loan Calculator FAQs

How to Calculate Monthly Payments for Commercial Loans

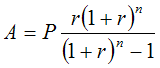

This commercial loan calculator uses the formula in the image to calculate the monthly payment for a commercial loan.

- A = Monthly payment amount

- P = Loan Principal

- r = Periodic interest rate

- n = Number of loan payments

How to use this commercial mortgage calculator

Enter your loan amount, estimated annual rate, and amortization term to instantly see your commercial loan payment. Toggle interest-only if applicable, adjust the payment frequency, and click calculate to refresh the amortization schedule. The rate tables above can help you choose a realistic starting point.

How long is a typical commercial mortgage?

Typically, the term (or length) of a commercial mortgage can be anywhere from 1-10 years, with limited exceptions for longer terms on self-amortizing loans such as SBA loans (up to 25 years), insurance or Fannie Mae loans (up to 30 years), or FHA loans (up to 35 years for refinance or 40 years for construction to permanent financing). However, the amortization schedule is typically longer than the 1-10 year loan term in order to keep the monthly payments affordable for the borrower.

How is interest calculated on a commercial loan?

This depends heavily on whether or not the loan is interest-only or amortizing. If it is interest only, the monthly interest is the rate divided by the number of periods in a year (i.e. 12), then multiplied by the loan amount. If it is an amortizing loan, the calculations are slightly trickier, and we recommend using a calculator like the one provided on this page.

How much interest will I pay on a commercial loan?

The interest paid on a commercial real estate loan will depend on the interest rate charged, the length of the term, and the amortization schedule. To see the total interest charged over time for any type of commercial loan, visit our calculator on this page and look at the "Total Interest" under the Payment Summary chart after inputting your loan amount, interest rate, and amortization.

How much do you have to put down on a commercial loan?

Your required down payment will ultimately depend on the purchase price, property or business cash flow, and loan program selected. However, you should typically expect to put down at least 10-15% on owner-occupied properties, 20-25% on apartment properties, and 25-30% on other types of investment properties.

How is commercial loan EMI calculated?

An EMI (equated monthly installment) is your monthly mortgage payment on a fixed-interest rate loan (i.e. the payment is the same every month). This can be easily estimated using the mortgage calculator on this page.

What is amortization and do commercial mortgages amortize?

An amortization schedule sets out the timeline for when the principal of the loan will be repaid and how much principal and interest will be included in each of your month mortgage payments. Unless you are on an interest-only loan (only available for construction, bridge, or low-leverage properties on certain loan products), all commercial mortgages amortize.

What are the qualifications for a commercial loan?

This will vary drastically by product, but the following are good rules of thumb regarding personal credit: 1) Net Worth equal to the loan amount being requested 2) Post-Closing Liquidity of at least 10% of the loan amount being requested (after the required down payment), FICO score of at least 680 with no recent negative credit events (i.e. collections, judgments, liens, bankruptcies, short sales, foreclosures, etc.), some (but not all) programs may require experience with similar properties or that you live within driving distance to the property.

What happens if you make extra payments on a commercial loan?

Making extra payments reduces your outstanding principal faster than the scheduled amortization. Each extra dollar lowers the balance on which future interest is calculated, so more of every subsequent payment goes toward principal. The result is a shorter payoff timeline and significantly less total interest paid. Use the Extra Monthly Payment toggle above to see exactly how many payments you save and how much interest you eliminate at your specific loan amount and rate.

How much interest can you save by making extra payments on a commercial loan?

The savings depend on your loan amount, interest rate, amortization term, and how early you begin making extra payments. Extra payments made early have the greatest impact because interest is front-loaded — a larger share of each early payment is interest. On a $2,000,000 loan at 7% amortized over 25 years, an extra $1,000 per month can eliminate hundreds of thousands of dollars in interest and cut years off the loan term. The amortization schedule above recalculates in real time when you enter an extra payment.

What is the difference between a loan term and amortization period on a commercial mortgage?

The loan term is the length of time before the loan matures and the remaining balance is due — typically 3 to 10 years for most commercial mortgages. The amortization period is the schedule over which monthly payments are calculated, often 20 to 30 years. Because the term is shorter than the amortization, most commercial loans end with a balloon payment — the remaining unpaid principal is due in full at maturity. Lenders typically expect borrowers to refinance or sell before that date.

How do you read a commercial loan amortization schedule?

Each row in the amortization schedule represents one payment period. The Payment column shows the total amount due. The Interest column shows how much covers interest on the outstanding balance. The Principal column shows how much reduces the loan balance. The Balance column shows the remaining principal after that payment is applied. Early in the loan, most of each payment is interest. Over time the interest portion shrinks and the principal portion grows — this shift is the defining characteristic of an amortizing loan.

Does making extra payments change the amortization schedule?

Yes. Extra principal payments cause the outstanding balance to drop faster than the original schedule assumes. Each subsequent interest charge is calculated on a lower balance, so more of each regular payment goes to principal. The schedule compresses — fewer total payments are needed to reach zero. The calculator above shows a revised amortization schedule automatically when you enter an extra monthly payment, so you can compare the standard and accelerated payoff side by side.

Can you pay off a commercial mortgage early?

Most commercial mortgages can be paid off before maturity, but prepayment is rarely free. Common penalties include step-down fees (a percentage that declines each year), yield maintenance (designed to make the lender whole on lost interest income), and defeasance (substituting government securities for the collateral). SBA and USDA loans have their own prepayment structures. Always review the prepayment clause in your loan documents before committing to an accelerated payoff strategy.

Note: The commercial mortgage calculators displayed in this website should be used as a guideline and do not represent a commitment to lend. Commercial Loan Direct and CLD Financial, LLC are not liable for any calculation errors resulting from the use of these calculators.